It’s time the mid-market accounting technology space woke up and realised its 2018. In Australia, MYOB have handed them the “goose that lays the golden eggs” with their decision not to take Single Touch Payroll to MYOB Premier (see my previous article) and yet none of them are in a position to genuinely capitalise, because they aren’t even playing the same game as the likes of Xero and Intuit!

Where are the bank feeds? How about a solid ecosystem of best of breed add-ons? How about AI and machine learning? How about a modern, mobile optimised UI with decent UX design? Why are these the domain of “small business” systems like Xero and QBo at one end and “corporate solutions” like Workday at the other? What happened in the middle?

A recent experience with a client (which is representative of what is going on in the broader mid-market) has really “got my goat” and compelled me to speak out!

But first, some background, for those who don’t know me or the accounting tech mid-market in Australia:

What do I know about the mid-market?

The last 18 years of my life has been spent, for the most part, working in the “mid-market” Accounting (and Payroll) Tech space.

- I have run and owned companies that fit the demographic and consumed the technologies as a user.

- I have sold accounting & payroll tech products and services to that market most of my career.

- I’ve been a shareholder and GM of a “leading” mid-market vendor.

- I have recommended and personally run implementations for literally hundreds of accounting & payroll system projects for mid-sized clients, through a couple of consulting businesses I have owned.

It is also fair to say I am a keen student of the accounting technology industry. I have spent a significant portion of my professional career studying the trends, hungry to understand the future. Researching local and foreign products and markets. Whilst not in the same league as the likes of Clayton Oates, Wayne Schmidt and Trent McLaren, I’ve attended my fair share of industry events around the world.

I also regularly put my thoughts out there, via my blog that focuses primarily on Australian and New Zealand accounting tech, for the world to consume and critique. I love to be challenged and am happy to admit error when made.

I’m no-longer young enough to think I know everything, but am forthright enough to retain an opinion built on experience.

What is the mid-market?

Whilst I’d often argue “mid-market” is a psychographic rather than a demographic, for simplicity I personally define the mid-market as servicing “mid-sized” organisations. Those which the ATO and ABS define as organisations, for profit or not, with more than 20 and generally less than 200 staff (though some industries, workforce sizes greater than 200 does not indicate business mindset of anything beyond a mid-sized business). And according to ABS stats, there’s around 50,000 of these in Australia (let’s throw in New Zealand and call it 60,000 in AuNZ). Typically, turnover is north of $3m and they have 3+ users of the core business system (industry dependent).

What is the state of the mid-market?

MYOB own the mid-market across Australia and New Zealand. And not because they have white-labeled Acumatica (as MYOB Advanced) or acquired Exo, Greentree, Pay Global, Commac, IMS etc etc. My research suggests that perhaps as much as 50% of organisations that fit the mid-sized demographic, still use MYOB (AccountRight) Premier Desktop (v19).

This is reflective of the low cloud penetration in this demographic. Whilst small and micro businesses have en masse adopted the cloud accounting tech solutions, mid-sized business, constrained by choice, fear and cost of change, sunk-cost fallacy, “functional parity” concerns and a dearth of quality advice have remained tied to ageing technology solutions.

Outside MYOB, and Reckon with Reckon (formerly QuickBooks Desktop) Premier and Enterprise, my estimate is, no one company owns more than 10% market share

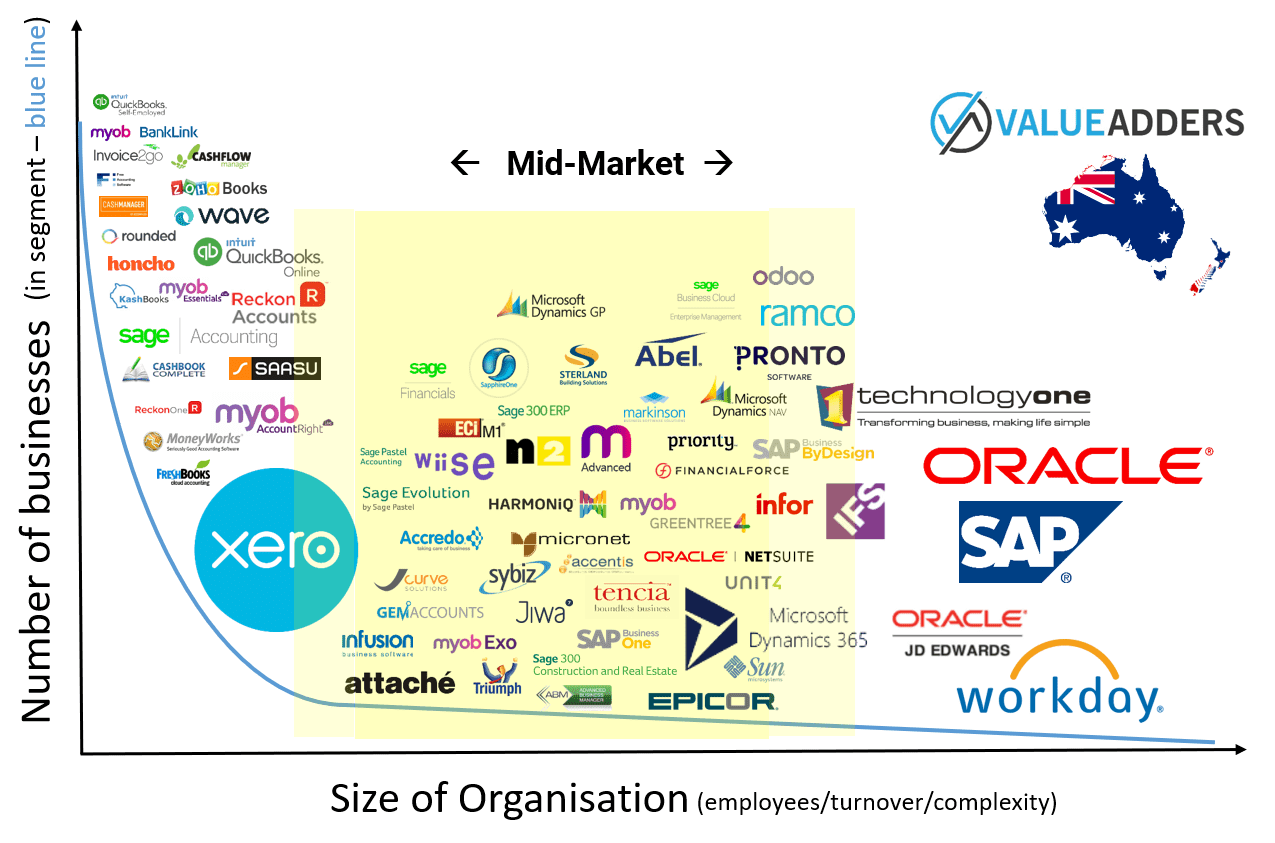

The above graphic is a rough, historically segmented view of the accounting technology industry across Australia and New Zealand according to target market (feel free to mention in a comment below any you think I have missed or got wrong).

Like MYOB, Reckon and Xero would certainly claim a fair stake in the mid-market, whilst few would acknowledge them as mid-market players as this has not been their target market.

Those specifically targeting mid-market include big international players (like Microsoft, Sage and NetSuite) and established/mature local players (like Attache, Pronto etc).

I must acknowledge that there are levels/subsets within the mid-market – solutions such as Pronto and Sage X3, are targeting very different price and functionality points to the likes of Attache or (NetSuite) JCurve.

For the most part, the majority of the players in this space over the past two decades, would tell you that their primary target audience would be conversions from MYOB Premier Desktop (the very product that is end of life and won’t be getting STP) or Reckon (QuickBooks) customers who had “outgrown” those “entry-level” / “small-business” solutions.

Setting the scene

With the background and market explained (from my perspective), today’s story begins with a phone call from a colleague I worked with a few years back. She wanted to validate the decision by her current employer, a Not-For-Profit, to move from Sage Timberline (aka 300 Construction & Real Estate) to MYOB Exo.

My response was simply “why on earth would you be looking at Exo over Advanced?”

To the chagrin of the Exo partners out there, I generally would not recommend someone implementing Exo in 2018. Happy to debate it with anyone, but the fact MYOB themselves use referrals to MYOB Advance + People towards accreditation BUT NOT Exo (nor Greentree, nor Pay Global), speaks volumes to where MYOB see their mid-market future.

A few months down the track, the same colleague calls asking me to validate the decision to go with MYOB Advanced + People. And this is really where my story begins. Because this time, my response was: “I need to understand the organisation, and your requirements before I can form an opinion and provide that advice“.

The process

Over the years I have built a 5 step process for small and medium organisations to choose and implement the right Accounting Tech: you can find a summary of the methodology here.

This case was slightly different as they were already effectively at “Step 4: Make a decision and commit to making it work” and very keen to not waste any more time revisiting steps 1-3 (out of frustration and confusion). They were hoping I would just say, yep, go for it, that’s the right investment decision!

So I go and see the team and discuss their:

- current state;

- desired state;

- non-negotiables;

- importants; and

- nice-to-haves.

Throw in a shortcut of my own experience with similar NFPs and we agree on the core requirements.

The core requirements

Without detailing everything, the situation can be summarised something like this:

- A mid-sized NFP with a seasonal, casual workforce, with a need for a decent payroll engine;

- Reporting against Budget and Actual by “job/project/event/segment” (whatever term you want to use), was at the heart of what they needed;

- Moderate, seasonal transaction volumes;

- There were 4 accounts and payroll staff on the existing accounting tech and 20 odd on the customised procurement system;

My advice

I’m not sure MYOB Advanced is the right investment. What it offers in terms of grunt and flexibility, is offset by the fact it is a comparatively harder-to-use system, that lacks bank feeds (despite MYOB owning BankLink, what the..?) and don’t get me started on the payroll solution MYOB People, which is highlighted by the fact timesheet costing doesn’t even flow through the accounting system and reporting…

It is also a significant investment for an NFP.

I follow this up with: what’s your thoughts on the likes of Xero and QBo?

The answer: they are small business solutions aren’t they, at that price point, we didn’t even look at them…

A fair and common response. In life, price frames quality perception. In business tech, price is often perceived as proportional to flexibility and capability, which to be fair has often been right.

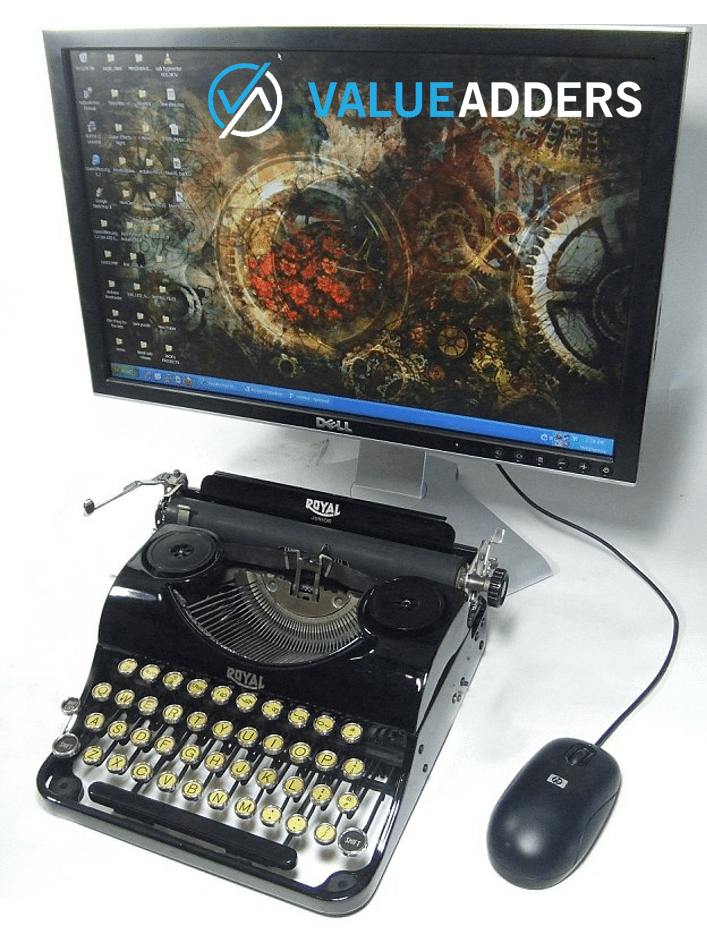

My typewriter explanation

Don’t confuse SME desktop accounting software with modern cloud platforms. Its like framing what a computer + a printer can do, based on experience with a typewriter. Yes they can output a page of prose, but if you think of a computer in terms of being limited to typing out and printing text, you are missing the point.

Such is small business accounting tech in the cloud vs desktop. Modern small business cloud platforms like Xero, QBo and even MYOB Essentials are built very differently to MYOB Premier (whose code base dates back to Macintosh computing in 1982) or QuickBooks Desktop (with its roots dating back to DOS in 1983 and Quicken). Technology has changed. Limitations aren’t what they used to be.

My Recommendation

A small business platform like Xero or QBo + add-ons (KeyPay + ApprovalMax) would not only deliver a far more cost effective solution, but I believe a better solution, one that is far more user friendly and with functionality such as bank feeds, a better payroll and workflow engine, more than exceeds the MYOB Advanced (and those of mid-market alternatives) offering for this organisation.

They still couldn’t believe that for a fraction of the licensing and implementation cost, they could get a system that met their needs, let alone a better system. So I arranged an end to end demo, using their data.

And the rest is history.

The response from the mid-market consultant

The client informed the competing VAR of their decision. And back comes a response, listing seven (7) reasons why what I had recommended can’t work.

And this is where I get exasperated!

Why is the same drivel I was using 10-15 years ago to convert MYOB Premier and QuickBooks (Reckon) desktop customers being trotted out in relation to Xero and QBo? I reiterate, the very category of small business software has changed.

I urge everyone do the research. Don’t believe the salesperson’s falsehoods.

Here are the 7 claims and the facts that refute them in 2018:

Claim 1: Transaction volumes – these smaller systems are just not designed for high transaction volumes…

The facts: Whilst Xero support do recommend transaction limits (which I suggest may predate their move to AWS and elastic computing…… I found this an interesting read), these limits are far greater than the client’s current and projected volume.

Intuit do not have transaction limits with QBo (explained here).

Claim 2: PO Authorisation – it is unlikely that you will be able to integrate a system like your procurement system or any other systems that may come along…

The facts: Really?? They clearly do not understand modern APIs (how are you selling Acumatica?) and how easy it is to integrate with the likes of Xero, QBo and MYOB small business products these days. And they clearly have not seen the likes of ApprovalMax, which come with “out-of-the-box” integration and workflows for Xero and QBo.

Claim 3: Reporting – can you do customised reporting?

The facts: Yes, and it was demonstrated with actual data… and if the standard reports weren’t good enough, there’s add-ons that offer enhanced, customised reporting!!! I seem to recall, PowerBI being a recommended add-on often with Acumatica… same applies to the likes of Xero, QBo and MYOB small business products, just that there are dozens of additional options as well!

Claim 4: Budgeting – small systems seldom have budgeting capabilities

The facts: which small packages could they possibly be talking about? Practically every GL on the market has budgets… And as for budget creation, most people, the reality is, want to use Excel. Beyond that there’s Castaway, Spotlight, Futrli etc, all integrated…

And if you mean in system budget creation tools, sure they can be sexy in the sales process, but rarely get used as everyone reverts to Excel!

Both Xero and QBo have great functionality around recording multiple budgets (to be frank, QBo better than Xero, with roll-up/dissected budgets, as opposed to independent budgets in Xero).

Claim 5: Audit trail – these systems lack comprehensive audit trails.

The facts: QBo has full audit trails (see this video). Xero’s audits are a WIP, but adequate, given the limited users who will actually accessing the system.

Claim 6: Project Tracking – would this have the capability and flexibility?

The facts: yep, both Xero and QBo now have projects and there are dozens of add-ons that also do that, best of breed, as good as or better than Acumatica!

Claim 7: Chart of Accounts – are in alpha format and are not flexible to provide the reporting you’ll need…

The facts: coding is optional, alpha or numeric, though the very notion is old-school to be frank. Reporting is not driven off the code structure, but the way in which you categorise the accounts. These system are easier to use and yet still relatively flexible with Class/Location/Tracking codes.

In closing

The reality is, whether it be an NFP, or a wholesale stock and debtors business, professional services or any other industry, SME cloud accounting platforms like Xero and QBo offer a serious and genuine alternative to mid-market ERP systems.

Decisions *should* be made:

- with acceptance that compromises will be needed, regardless of the solution selected;

- on a ROI basis;

- on a feature for feature comparison, with significant value placed on the user experience design and ease of use (believe me, this is important to the modern workforce comprised increasingly of Millennials);

- with weighting the value one places on “one-throat-to-choke all-in-one solution” vs a “best-of-breed” integrated system;

Decisions *should not* be made, based:

- on believing a sales person or consultant with out-dated market knowledge;

- on historical separations between market segments or historical technical limitations of SME solutions of the past;

- the misnomer that price equates proportionally to features and functions, or value delivered;

- on the belief that a perfect solution exists;

And for what it is worth, in my mind, the 2 key reasons to look at ERP over the likes of Xero and QBo + addons are:

- Multi and inter-entity management & processing;

- The desire to have Finance & CRM on one platform;

___

For more on Accounting, Payroll & HR tech:

Follow On Twitter: https://twitter.com/mattpaff and https://twitter.com/valueadders

Follow our Blog: https://valueadders.com.au/articles/

Follow our LinkedIn: https://www.linkedin.com/company/value-adders/

Like on Facebook: https://www.facebook.com/valueadders/

Follow on Medium: https://medium.com/@mattpaff

Glad to hear Intuit and other mid-sized accounting software solutions are coming to markets around the world. I love my AMS accounting and payroll software and tell people all the time that I’m getting a mid-sized business solution at a small business price. These systems can really save accounting teams valuable time.

What impact do you feel GreatSoft might have, Matt?

I started in the accounting tech industry as the assistant to the export manager at Attaché 18 years ago. The first outbound call I ever made was to Bruce Morgan at Greatsoft! I’ve stayed in touch with Bruce ever since and think timing is right, with Brian now on board, they will smash it I reckon (pun intended)!